What is car equity? Car equity is the difference between your car’s current market value and the amount you still owe on your car loan. Can I use my car equity? Yes, you can use your car equity for various financial purposes, such as a down payment on a new car, paying off other debts, or even accessing it through a vehicle equity loan.

Knowing the equity in your car is a crucial step if you’re considering selling your vehicle, trading it in, or using it as collateral for a loan. It’s not as complicated as it might sound, and with a few simple steps, you can accurately determine your car’s financial standing. This guide will walk you through the process, making it easy to grasp.

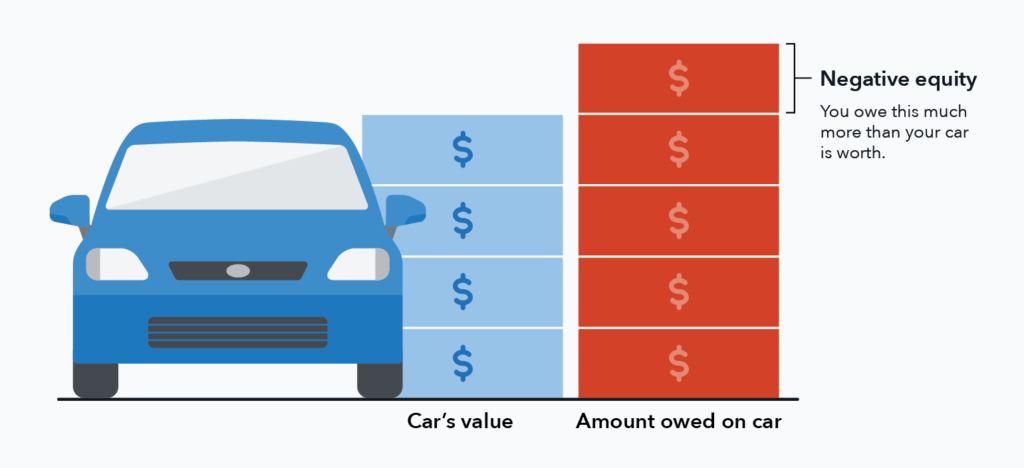

Image Source: canadianautobrokers.ca

Figuring Out Your Car’s Value

The first pillar of calculating car equity is knowing what your car is worth today. This isn’t what you paid for it, but what a buyer would likely offer you right now. Several reliable sources can help you with this.

Using Online Car Value Estimators

The quickest way to get an idea of your car’s worth is by using online car value estimator tools. These websites are designed to give you a market-based price for your vehicle.

- Kelley Blue Book (KBB): KBB is a well-known and trusted source. You input your car’s year, make, model, trim, mileage, and condition, and it provides a range of values.

- Edmunds: Similar to KBB, Edmunds offers a comprehensive valuation tool. They often provide different values for private party sales and trade-ins.

- NADA Guides: NADA (National Automobile Dealers Association) also offers vehicle valuation, often used by dealerships and financial institutions.

When using these estimators, be as honest as possible about your car’s condition. Factors like dents, scratches, interior wear and tear, and even recent maintenance can significantly impact the value. You’ll usually get a few different price points:

- Retail Value: What a dealer would likely sell a similar car for.

- Trade-in Value: What a dealer might offer you if you trade your car in towards a new purchase.

- Private Party Value: What you might get if you sell your car directly to another individual.

For a realistic picture of your net equity in vehicle, the private party value is often the most useful if you plan to sell it yourself, while the trade-in value is key if you’re dealing with a dealership.

Factors Affecting Your Car’s Market Value

Several things influence how much your car is worth:

- Mileage: Higher mileage generally means lower value.

- Condition: Excellent condition (mechanical and cosmetic) commands a higher price. Regular maintenance is key.

- Age: Older cars typically depreciate more.

- Make and Model: Some brands and models hold their value better than others.

- Features and Options: Premium sound systems, sunroofs, advanced safety features, and navigation systems can add value.

- Accident History: A clean history is essential. Cars with previous accidents, especially major ones, will be worth less.

- Demand: The current market demand for your specific type of vehicle plays a role. For example, fuel-efficient cars might be in higher demand when gas prices are high.

Calculating Your Car Loan Balance

The other critical piece of the puzzle is how much you owe on your car loan. This is your loan payoff amount. Knowing this precisely is vital.

Obtaining Your Loan Payoff Amount

Your loan payoff amount is not simply the total amount of your loan divided by the number of payments. It includes the principal balance plus any accrued interest up to the point you plan to pay it off, and sometimes even a small fee for an early payoff.

- Contact Your Lender: The most accurate way to get your loan payoff amount is to call your auto loan lender directly. Ask for your “payoff quote.” They will provide a specific dollar amount that is valid for a certain period (usually 10-15 days).

- Check Your Online Account: Many lenders allow you to access your loan details through an online portal. You can often find your current balance and sometimes a payoff quote there.

- Review Your Monthly Statements: Your monthly statements will show your current principal balance, but it’s always best to get an updated payoff quote directly from the lender.

Important Note: When you request a payoff quote, make sure to ask if it includes any penalties for paying off the loan early. Most modern auto loans do not have prepayment penalties, but it’s always good to confirm.

The Car Equity Calculation: Putting It Together

Now that you have both your car’s estimated market value and your loan payoff amount, you can perform the car equity calculation.

The Formula for Car Equity

The formula is straightforward:

Car Equity = Current Market Value of Your Car – Loan Payoff Amount

Let’s break this down with an example:

- Estimated Market Value (Private Party Sale): $18,000

- Loan Payoff Amount: $12,000

Car Equity = $18,000 – $12,000 = $6,000

In this scenario, you have $6,000 in equity in your vehicle. This means if you were to sell your car for its estimated market value and pay off the loan, you would walk away with $6,000 in cash.

What Does Positive vs. Negative Equity Mean?

- Positive Equity: When your car’s market value is greater than your loan payoff amount, you have positive equity. This is the ideal situation, giving you financial flexibility.

- Negative Equity (Upside Down): When your loan payoff amount is greater than your car’s market value, you have negative equity. This means you owe more than the car is worth. For instance, if your car is worth $10,000 but you owe $13,000, you have -$3,000 in equity. This can make selling or trading in your car more complicated.

Scenarios for Using Your Car Equity

Understanding your car equity opens up various financial possibilities.

Trading In Your Car

When you trade in your car at a dealership, the dealer will offer you a trade-in value. This value is then used to reduce the price of the new car you’re purchasing.

Let’s say you’re trading in a car with a trade-in value of $15,000 and you owe $10,000 on it.

- Your Equity: $15,000 (Trade-in Value) – $10,000 (Loan Payoff) = $5,000

This $5,000 in equity acts as a down payment towards your new car. If the new car costs $30,000, you would essentially owe $25,000 on it after the trade-in. This significantly reduces your new car loan amount and your monthly payments.

Selling Your Car Privately

A private car sale equity usually results in a higher sale price than a trade-in because you’re not dealing with a dealership’s markup. If your car is worth $18,000 on the private market and you owe $12,000:

- Your Equity: $18,000 (Private Party Value) – $12,000 (Loan Payoff) = $6,000

After selling your car and paying off the loan, you would have $6,000 in cash. However, selling privately requires more effort, including advertising, showing the car, and handling paperwork.

Selling Car With Loan

It is entirely possible to be selling car with loan, even if you have negative equity. If you owe $13,000 on a car worth $10,000, and a buyer offers $10,500, you’ll need to come up with the difference of $2,500 ($13,000 – $10,500) to pay off the loan. You would still need to cover this difference from your own funds before the title can be transferred.

Vehicle Equity Loan or Cash-Out Refinance

If you have significant positive equity in your car, you might be able to tap into it.

- Vehicle Equity Loan: This is a type of secured loan where your car’s equity serves as collateral. You receive a lump sum of cash based on your equity.

- Cash-Out Refinance: You refinance your existing auto loan for a larger amount than you currently owe and receive the difference in cash.

These options can be beneficial for consolidating debt, covering unexpected expenses, or funding a large purchase. However, remember that if you default on these loans, the lender can repossess your vehicle.

Car Financing Options and Equity

When you are looking at new car financing options, your existing car equity can be a valuable asset.

- Down Payment: As mentioned, positive equity directly translates into a larger down payment for your next vehicle. This can lower your monthly payments, reduce the total interest paid over the life of the loan, and potentially help you qualify for a better interest rate.

- Trade-in Value: Dealers use the trade-in value of your current car to offset the cost of the new one.

- Avoiding Negative Equity: If you have substantial negative equity, you might consider paying off the difference before trading in or selling, if possible, to avoid rolling that debt into a new loan.

Tips for Maximizing Your Car’s Value

To ensure you get the most accurate valuation and the best possible equity, consider these tips:

Maintain Thorough Records

Keep detailed records of all maintenance and repairs. This includes oil changes, tire rotations, brake jobs, and any significant repairs. A well-documented history builds buyer confidence.

Keep Your Car Clean and Well-Maintained

- Regular Washes and Waxes: Protects the paint and keeps the exterior looking good.

- Interior Cleaning: Vacuum carpets, clean upholstery, and wipe down surfaces regularly. A clean interior makes a big difference.

- Address Minor Issues: Fix small dents, scratches, or chips as soon as possible.

- Mechanical Check-ups: Ensure all systems are running smoothly. This includes checking tire pressure, fluid levels, and lights.

Be Honest About Condition

While you want to present your car in the best light, being upfront about any issues can prevent problems during the sale or trade-in process. It builds trust.

Research the Market

Before listing your car or visiting a dealership, do your homework on what similar vehicles are selling for in your area. This helps you set a realistic price and negotiate effectively.

Frequently Asked Questions (FAQs)

Q1: What is the difference between trade-in value and private party value?

A1: The trade-in value is the amount a dealership will offer you when you trade your car in towards a new purchase. This is typically lower than the private party value because the dealer needs to make a profit on resale. The private party value is what you can expect to get if you sell your car directly to another individual.

Q2: Can I sell my car if I still have a loan on it?

A2: Yes, you can sell your car even if you still have a loan. However, the process is slightly more complex. You will need to pay off the outstanding loan balance using the sale proceeds. If the sale price is less than the loan balance (negative equity), you’ll need to pay the difference out of pocket.

Q3: How long does it take to get a car equity loan?

A3: The time it takes to get a vehicle equity loan can vary depending on the lender and the complexity of the application. Typically, it can take anywhere from one to a few business days after your application is approved.

Q4: What is considered “good” car equity?

A4: Having positive equity in your car is generally considered good. The more positive equity you have, the more financial flexibility you gain. For example, having equity equal to 20% or more of your car’s value is often seen as a strong position.

Q5: If my car has negative equity, can I still get a new car loan?

A5: Yes, it is often still possible to get a new car loan even with negative equity. However, lenders may require a larger down payment to offset the negative equity, and you might face higher interest rates due to the increased risk. Some lenders might allow you to roll the negative equity into the new loan, but this will increase your overall loan amount and monthly payments.

By following these steps, you can confidently determine your car’s equity and make informed decisions about your automotive finances.