Yes, you can absolutely trade in a financed car for another car. This process involves using the trade-in value of your current financed vehicle to offset the cost of a new or used car. The key lies in understanding your current loan’s status and the potential equity you have in your vehicle.

Trading in a car you still owe money on is a common practice, and many people navigate it successfully. It might seem complex at first, especially with the outstanding car loan trade in element, but with a clear understanding of the steps involved, it can be a smooth transition to a new vehicle. This guide will walk you through the entire dealership trade in process for a financed car, from calculating your car’s worth to driving away in your next set of wheels.

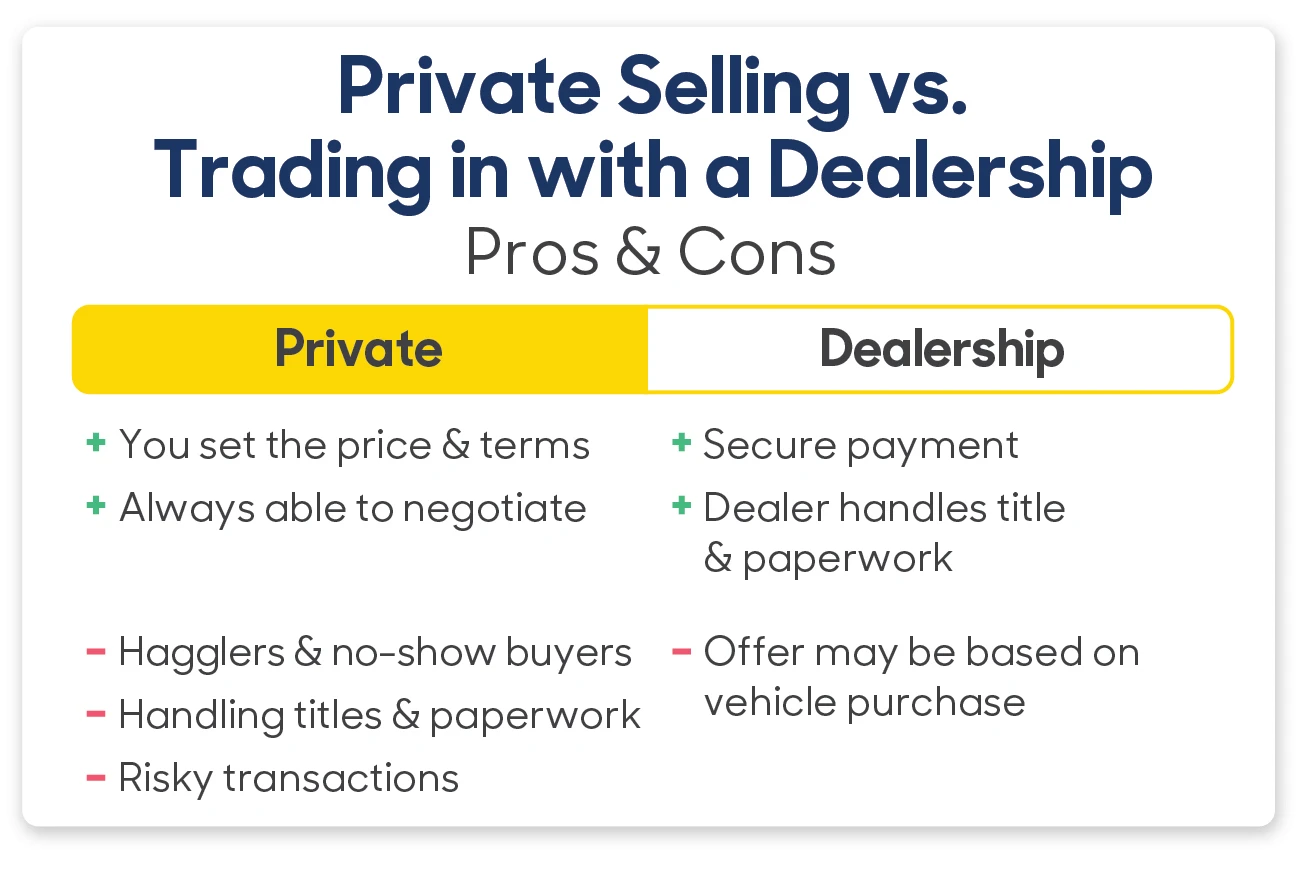

Image Source: content-images.carmax.com

Deciphering Your Current Car Loan

Before you even set foot on a dealership lot, the first crucial step is to get a handle on your current auto loan. This isn’t just about knowing your monthly payment; it’s about knowing the precise amount you still owe.

Obtaining Your Payoff Amount

To effectively trade in a financed car, you need to know the exact amount required to payoff car loan. This figure is not the same as your outstanding balance on a statement. It includes any remaining principal, accrued interest, and potentially any early termination fees.

How to get your payoff amount:

- Contact your lender: This is the most direct and accurate method. Call your bank or credit union and ask for a “payoff quote.” They will typically provide you with a quote that is valid for a specific period, usually 10 to 30 days.

- Check your online account: Many lenders offer online portals where you can view your loan details, including the current payoff amount.

- Review your loan documents: While this might give you an idea of your initial loan, it’s best to get an updated payoff quote directly from your lender.

This payoff quote is your golden ticket. It’s the number you need to compare against your car’s trade-in value.

Evaluating Your Car’s Trade-In Value

Your car’s value is central to the entire trading in a car with a loan equation. You need to know what your car is worth in the current market to determine if you have positive or negative equity.

Researching Market Prices

Several resources can help you estimate your car’s trade-in value:

- Online Valuation Tools: Websites like Kelley Blue Book (KBB), Edmunds, and NADA Guides offer free tools to estimate your car’s worth. They consider your car’s make, model, year, mileage, condition, and even your zip code. Be sure to check the “trade-in” value, which is generally lower than the “private party” or “retail” value.

- Dealership Websites: Many dealerships also provide online trade-in valuation tools. These can offer a good starting point, but remember they are often estimations.

- Local Market Research: Look at similar vehicles for sale at local dealerships or on online marketplaces. This can give you a real-world sense of what buyers are paying.

When using these tools, be honest about your car’s condition. Minor wear and tear can significantly impact the value.

Factors Influencing Trade-In Value:

- Make and Model: Some brands and models hold their value better than others.

- Mileage: Lower mileage generally means a higher value.

- Condition: Dents, scratches, interior wear, and mechanical issues will reduce the value.

- Vehicle History: Accidents, title issues (like salvage or flood damage), and frequent repairs can lower the value.

- Features and Options: Higher trim levels and desirable features (like leather seats, sunroofs, navigation) can increase value.

- Market Demand: Popularity of certain vehicles in your region plays a role.

Comprehending Equity in Your Financed Car

Equity is the difference between what your car is worth and what you owe on the loan. This is the most critical factor when trading in a car with a loan.

Positive Equity vs. Negative Equity

-

Positive Equity: This occurs when your car’s trade-in value is higher than your payoff car loan amount. For example, if your car is worth $12,000 and you owe $9,000, you have $3,000 in positive equity. This positive equity can be used as a down payment on your next car, reducing the amount you need to finance. This is often referred to as positive equity car trade in.

-

Negative Equity (Upside Down): This happens when your car’s trade-in value is lower than your payoff car loan amount. If your car is worth $8,000 but you owe $10,000, you have $2,000 in negative equity. This means you still owe $2,000 after trading in your car. This situation is also known as negative equity trade in.

Calculating Your Equity

The calculation is straightforward:

Car’s Trade-In Value – Payoff Amount = Net Equity

- Positive Net Equity: If the result is a positive number, you have equity.

- Negative Net Equity: If the result is a negative number, you have negative equity. This is what is meant by the net equity trade in value.

How Does Trading In A Financed Car Work? The Dealership’s Role

When you decide to trade in a financed car, the dealership plays a pivotal role in facilitating the transaction. They essentially handle the payoff of your old loan and integrate the remaining balance (or credit) into your new car deal.

The Dealership Trade-In Process

Here’s a step-by-step look at how does trading in a financed car work at a dealership:

- Vehicle Assessment: The dealership will inspect your current car to determine its trade-in value. This assessment often involves a test drive and a thorough inspection of its condition.

- Offer Presentation: They will present you with a trade-in offer based on their assessment and market research.

- Loan Payoff: If you accept the offer and decide to proceed, the dealership will use the trade-in value to pay off your existing car loan directly to your lender.

-

New Car Purchase:

- Positive Equity: If your trade-in value exceeds your payoff amount, the difference (your positive equity) will be applied as a down payment towards your new car purchase. This reduces the amount you need to finance for the new vehicle.

- Negative Equity: If your trade-in value is less than your payoff amount, the dealership will “roll over” the remaining balance of your old loan into your new car loan. This means you’ll be financing the cost of the new car plus the amount you still owe on the old one.

-

New Loan Arrangement: You will then arrange financing for the new car, taking into account any applied equity or rolled-over negative equity.

The Scenario of Rolling Over a Car Loan

Rolling over car loan debt is a common outcome when dealing with negative equity. It essentially means the remaining debt from your old car loan is added to the loan for your new car.

Example of Rolling Over a Car Loan:

- You owe $10,000 on your current car.

- The dealership offers you $8,000 for your trade-in.

- This leaves you with $2,000 in negative equity.

- You want to buy a new car for $25,000.

In this scenario, your new car loan would be for $25,000 (new car cost) + $2,000 (rolled-over negative equity) = $27,000.

Pros of Rolling Over:

- Allows you to get out of your current car, even with negative equity.

- Enables you to drive away in a new vehicle without having to come up with cash for the shortfall.

Cons of Rolling Over:

- You will pay interest on the negative equity amount, increasing the total cost of your new car loan.

- You start your new car loan “upside down” again, meaning you owe more than the car is worth from the outset.

- Your monthly payments for the new car will be higher than if you had no negative equity.

Navigating the Negotiation

Negotiating your trade-in value is a crucial part of the process. The initial offer from a dealership is often just a starting point.

Strategies for a Better Trade-In Value

- Be Prepared: Know your car’s estimated value before you go to the dealership. Bring printouts from KBB, Edmunds, etc.

- Know Your Payoff: Have your exact payoff amount readily available.

- Independent Appraisal: If you’re not happy with the dealership’s offer, consider getting an appraisal from another dealership or a service like CarMax. This can provide leverage in your negotiation.

- Negotiate the New Car Price First: It’s often recommended to finalize the price of the new car before discussing your trade-in. This prevents the dealership from manipulating figures between the two transactions.

- Consider Selling Privately: While more effort, selling your car privately often yields a higher price than trading it in. If you have significant positive equity or a substantial amount of negative equity, this might be a worthwhile option.

When to Walk Away

If the dealership’s offer is significantly lower than market value, or if they are unwilling to negotiate, be prepared to walk away. There are other dealerships, and other ways to sell your car.

The Paperwork and Finalizing the Deal

Once you’ve agreed on a price for the new car and the trade-in value, it’s time to handle the paperwork.

Key Documents to Review

- Bill of Sale: This document details the purchase of the new vehicle, including the agreed-upon price, any fees, and taxes.

- Trade-In Agreement: This outlines the trade-in value of your current vehicle and how it’s being applied (e.g., as a down payment or to cover negative equity).

- Loan Documents: If you’re financing the new car, you’ll review and sign the loan agreement, which details the interest rate, loan term, and monthly payments.

- Title and Registration: You’ll need to sign over the title of your old car to the dealership. The dealership will then handle the new registration and title for your new vehicle.

Ensuring Your Old Loan is Closed

It’s essential to confirm with your old lender that your loan has been fully paid off by the dealership. You should receive confirmation and any necessary documentation, such as a lien release, within a reasonable timeframe.

Alternatives to Trading In

While trading in a financed car is common, it’s not the only option, especially if you have significant negative equity or want to avoid the complexities.

Selling Your Car Privately

As mentioned, selling your car yourself can often result in a higher sale price than a trade-in.

Steps for Private Sale:

- Pay off your loan: You’ll need to pay off your loan first. If you have positive equity, the sale proceeds will cover the loan, and you’ll pocket the difference. If you have negative equity, you’ll need to come up with the difference in cash to pay off the loan before you can sell the car.

- Prepare the car: Clean it thoroughly, fix any minor issues, and gather all maintenance records.

- Advertise: Use online platforms like Craigslist, Facebook Marketplace, eBay Motors, or local classifieds.

- Screen buyers: Be cautious of scams. Meet in safe, public places.

- Handle paperwork: Once a buyer is found, you’ll complete the sale paperwork and ensure the title is transferred correctly.

Selling to a Non-Dealership Buyer

Services like CarMax or Carvana will buy your car outright, often providing competitive offers. They handle the payoff of your loan directly. This can be a good middle ground if you want the convenience of a dealership transaction but a potentially better price than a traditional trade-in.

Frequently Asked Questions (FAQ)

Here are some common questions about trading in a financed car:

Q1: Can I trade in a car with a loan even if I have negative equity?

A1: Yes, you can trade in a car with a loan even if you have negative equity. The dealership will roll the outstanding negative balance into your new car loan, or you may be required to pay the difference in cash.

Q2: What is “rolling over” a car loan?

A2: “Rolling over” a car loan refers to adding the remaining balance of your old car loan to the new car loan when you have negative equity.

Q3: How do I know if I have equity on a financed car?

A3: You have equity on a financed car if its current market trade-in value is more than the amount you owe on the car loan.

Q4: What happens if my trade-in value is less than my payoff car loan?

A4: If your trade-in value is less than your payoff car loan, you have negative equity. This difference will need to be addressed, usually by adding it to your new car loan or paying it in cash.

Q5: Is it a good idea to roll over negative equity into a new car loan?

A5: While it allows you to get a new car without upfront cash for the shortfall, rolling over negative equity means you’ll pay more in interest over the life of the loan and start your new loan upside down. It’s generally advisable to avoid if possible.

Q6: Can I trade in a car that is only a few months old?

A6: Yes, you can trade in a car that is only a few months old. However, due to rapid depreciation, you are more likely to have negative equity on a nearly new vehicle, especially if you financed a significant portion of its cost.

Q7: What is the net equity trade in value?

A7: The net equity trade in value is the difference between your car’s trade-in value and the total amount you owe on your car loan. A positive number indicates equity, while a negative number indicates negative equity.

By thoroughly researching your car’s worth, understanding your loan’s specifics, and being prepared for negotiations, you can successfully navigate the process of trading in a financed car for your next vehicle.