Can you trade in a car with negative equity? Yes, you can trade in a car with negative equity, but it requires careful planning and may involve additional costs. This guide will walk you through the process of dealing with negative equity car situations and how to navigate them when you’re looking to get a new car.

Many people find themselves in the unenviable position of owing more on their car loan than the car is actually worth. This is known as negative equity, and it can feel like a financial roadblock, especially when you’re eager to upgrade to a new vehicle or your current car is no longer meeting your needs. Fortunately, it’s not an insurmountable problem. This comprehensive guide will equip you with the knowledge and strategies to successfully trade in your car with negative equity, covering everything from understanding the problem to finding solutions.

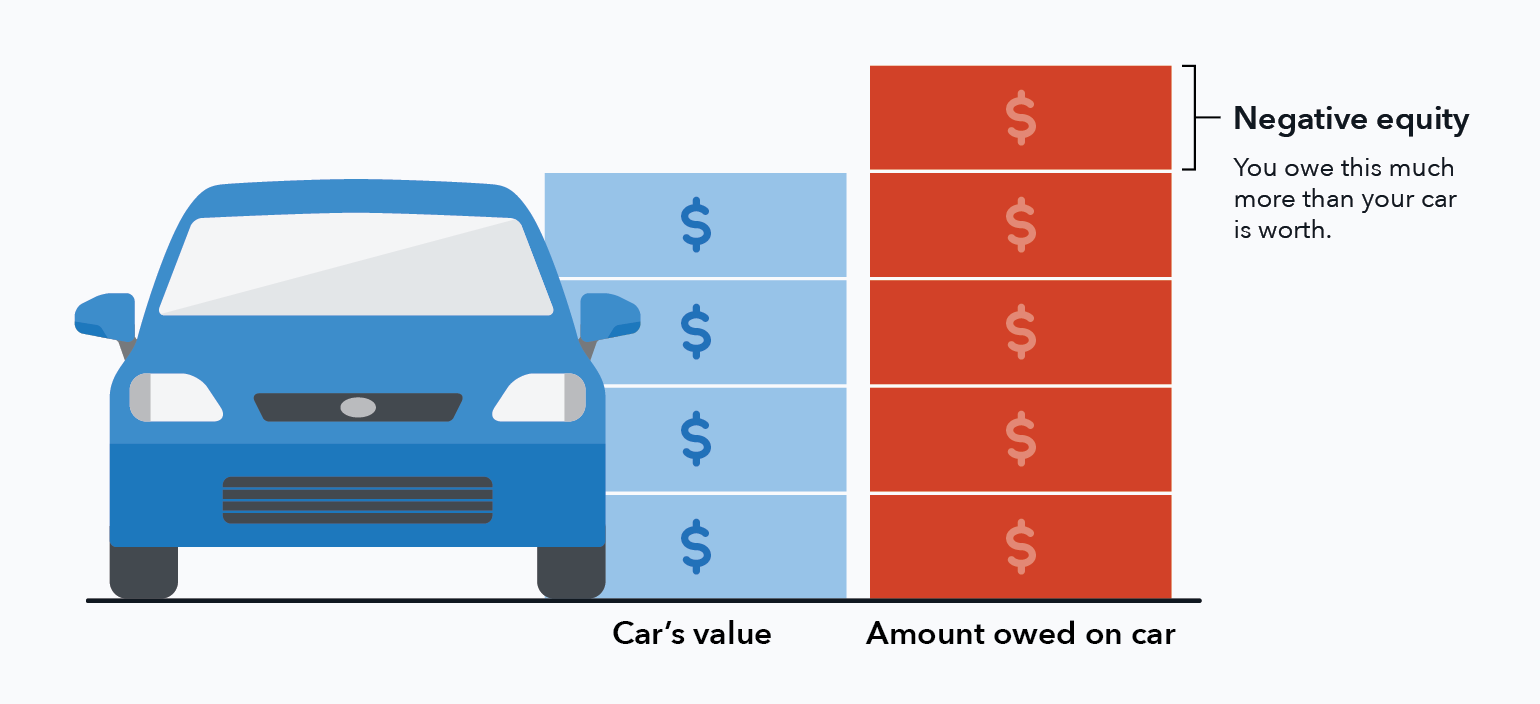

Image Source: files.consumerfinance.gov

Deciphering Negative Equity

Before diving into the how-to, it’s crucial to grasp what negative equity truly means.

What is Negative Equity?

Negative equity occurs when the outstanding balance on your car loan is greater than the car’s current market value. This is common with new cars, which depreciate significantly in their first few years, and can be exacerbated by high interest rates, long loan terms, or making a very small down payment.

Why Does Negative Equity Happen?

Several factors contribute to a car falling into negative equity:

- Rapid Depreciation: New cars lose a substantial portion of their value as soon as they are driven off the lot. This depreciation often outpaces loan payments, especially in the early years of the loan.

- Long Loan Terms: Longer loan periods mean you’re paying more interest over time, and it takes longer to build equity in the vehicle.

- Low Down Payments: A smaller initial investment means you start with a larger loan balance, making it easier to owe more than the car is worth.

- High Interest Rates: A higher Annual Percentage Rate (APR) means more of your monthly payment goes towards interest rather than principal, slowing down equity building.

- Bad Credit: If you have poor credit, you might have received a loan with a higher interest rate, increasing the likelihood of negative equity.

- Accidents or Damage: Significant damage that isn’t fully covered by insurance can drastically reduce a car’s value, potentially creating negative equity.

The Challenges of Trading in a Car with Negative Equity

Trading in a car when you owe more than it’s worth presents several hurdles that you’ll need to overcome.

The Impact on Your New Car Purchase

When you trade in a car with a car trade-in negative balance, the dealership will typically pay off your existing loan. If the amount they offer for your trade-in is less than your loan payoff amount, the difference becomes a debt you still owe. This shortfall is then usually rolled into your new car loan.

This means you’ll be financing not only your new car but also the remaining balance from your old car. This can lead to:

- Higher Monthly Payments: A larger overall loan amount naturally translates to higher monthly payments.

- More Interest Paid: Financing the negative equity means you’ll pay interest on that amount as well, increasing the total cost of your new vehicle.

- Increased Risk of Future Negative Equity: Starting your new car loan with a larger balance makes it more likely you’ll fall into negative equity again in the future.

Strategies for Selling Car With Loan Negative

Even with negative equity, there are actionable steps you can take to manage the situation effectively.

Strategy 1: Pay Down the Difference Out-of-Pocket

The most straightforward way to handle negative equity is to pay the difference between your car’s value and your loan balance in cash.

How it works:

- Determine Your Car’s Value: Get an accurate estimate of your car’s current market value from reputable sources like Kelley Blue Book (KBB), Edmunds, or NADA Guides. Also, get quotes from multiple dealerships and online car buying services (e.g., Carvana, Vroom).

- Find Your Loan Payoff Amount: Contact your lender for the exact amount you owe on your loan.

- Calculate the Shortfall: Subtract your car’s estimated value from your loan payoff amount. If the result is positive, that’s your negative equity.

- Pay the Difference: If you have the funds, you can pay this shortfall directly to your lender before or at the time of the trade-in.

Pros:

- Avoids rolling the debt into a new loan.

- Results in lower monthly payments on your new car.

- Saves money on interest over the long term.

- Helps you get out of car negative equity faster.

Cons:

- Requires having a significant amount of cash available.

Strategy 2: Negotiate a Better Trade-in Value

Dealerships are businesses, and there’s often room for negotiation.

How it works:

- Shop Around: Get quotes from multiple dealerships. Knowing what other dealers are offering can give you leverage.

- Highlight Your Car’s Strengths: If your car is in excellent condition, has low mileage, and desirable features, emphasize these points.

- Be Prepared to Walk Away: If the offer doesn’t meet your needs, don’t be afraid to leave.

Strategy 3: The “Upsizing” Approach with a Specific Goal

Sometimes, upsizing car negative equity can be a calculated move if it allows you to achieve a specific financial goal. This involves trading in your current car with negative equity for a newer, potentially more fuel-efficient or reliable vehicle, with the expectation that the depreciation curve on the new car will be less steep or that the loan terms will be more favorable.

How it works:

- Target a Car with Lower Depreciation: Research vehicles that historically hold their value well.

- Secure Favorable Financing for the New Car: A good credit score and a substantial down payment (even if it means using savings) on the new car are crucial.

- Calculate the Total Cost: Ensure the increased monthly payment and interest are manageable and that the benefits of the new car outweigh the cost of carrying over negative equity.

Pros:

- Can lead to a more reliable or suitable vehicle.

- Potentially better fuel economy or lower maintenance costs.

Cons:

- Still involves rolling debt into a new loan.

- Requires careful financial calculation to ensure it’s a sound decision.

Strategy 4: Seek a Loan Payoff Car Trade-in Solution

When you’re looking to sell your car and pay off the existing loan, you might be able to find specific programs or dealership incentives designed to help with situations like yours. This is a direct approach to a loan payoff car trade-in.

How it works:

- Ask Dealerships Directly: Inquire if they have any programs that assist customers with negative equity when trading in their vehicles.

- Explore Manufacturer Incentives: Sometimes, manufacturers offer incentives that can help offset the cost of a new vehicle, which might indirectly help with negative equity.

Strategy 5: Car Refinancing Negative Equity (Indirectly)

While you can’t directly refinance the negative equity portion of your loan into your new car loan without it being rolled over, exploring car refinancing negative equity on your current vehicle before trading it in can sometimes be an option, though often not practical. This is usually more about restructuring your current debt to free up cash or lower payments, which might help you save enough to pay down the negative equity before trading.

How it works:

- Refinance Your Current Car Loan: If you can secure a lower interest rate or a longer term on your current loan, it might lower your monthly payments, freeing up cash. However, this doesn’t eliminate the negative equity itself.

- Use Savings to Pay Down the Principal: The cash saved from refinancing could be used to pay down the principal on your current loan, reducing the negative equity before you trade.

Pros:

- Potentially lowers current monthly payments.

- Could free up cash to pay down negative equity.

Cons:

- Does not eliminate negative equity; it just restructures the debt.

- May not be possible if your credit has worsened or the car’s value has dropped further.

- Can extend the loan term, leading to more interest paid overall.

Strategy 6: Sell the Car Privately

Selling your car yourself, rather than trading it in, often yields a higher selling price. This can help you recoup more of the car’s value and reduce your negative equity.

How it works:

- Price Your Car Competitively: Research private party values on KBB, Edmunds, etc.

- Prepare Your Car: Clean it thoroughly, fix minor cosmetic issues, and gather all maintenance records.

- Advertise Your Car: Use online platforms like Craigslist, Facebook Marketplace, AutoTrader, or eBay Motors.

- Negotiate with Buyers: Be prepared to negotiate on price.

- Handle the Loan Payoff: Once you have a buyer, you’ll need to coordinate paying off the loan. This might involve meeting at your bank or lender’s branch to ensure the title is transferred cleanly. You will still need to cover the difference between the sale price and the loan payoff if there’s a shortfall.

Pros:

- Typically fetches a higher price than a trade-in.

- Gives you more control over the sale process.

- Maximizes your chances of reducing car debt trade-in by getting a better price.

Cons:

- Time-consuming and requires effort.

- You’ll need to handle all advertising, showings, and negotiations.

- Potential safety concerns when meeting strangers.

- You still need to cover any negative equity yourself.

Strategy 7: Consider Transferring Negative Equity (Rare and Risky)

In very specific circumstances, a dealership might consider transferring negative equity loan into a new loan for a different vehicle, essentially rolling it over. However, this is becoming less common and often comes with unfavorable terms.

How it works:

- This usually only happens if you are buying a more expensive vehicle and the dealership is willing to absorb some of the loss or if their financing partners allow it under specific conditions. It’s crucial to scrutinize the terms of any such arrangement.

Pros:

- Allows you to get a new car without paying the negative equity upfront.

Cons:

- Significantly increases your new car loan amount and monthly payments.

- Leads to paying more interest over the life of the loan.

- Can trap you in a cycle of debt.

Strategy 8: The “Out of Car Negative Equity” Accelerator

This is a proactive approach focused on aggressively paying down your current car loan to get out of car negative equity before trading.

How it works:

- Make Extra Payments: Allocate any extra income (bonuses, tax refunds) towards your car loan principal.

- Bi-Weekly Payments: If your lender allows, paying half your monthly payment every two weeks can result in one extra monthly payment per year, accelerating payoff.

- Cut Expenses: Temporarily reduce discretionary spending to put more money towards your loan.

Pros:

- Reduces the amount of negative equity you’ll need to address.

- Saves money on interest.

- Improves your financial health.

Cons:

- Requires discipline and financial sacrifice.

- May take time to significantly reduce negative equity.

Preparing for the Trade-In

Once you’ve chosen a strategy, preparation is key to a smoother transaction.

Vehicle Condition

- Cleanliness: A detailed interior and exterior can significantly impact a car’s perceived value. Wash, wax, and vacuum your car thoroughly.

- Minor Repairs: Fix small issues like cracked taillights, burnt-out bulbs, or chipped paint if the cost is minimal compared to the potential increase in value.

- Maintenance Records: Having a log of regular maintenance and repairs shows you’ve taken good care of the vehicle.

Documentation

- Loan Payoff Statement: Your lender should provide this.

- Title and Registration: Ensure you have these readily available. If your loan is still active, the lender will typically hold the title.

- Maintenance Records: As mentioned above.

Getting a New Car with Negative Equity

When you’re getting new car negative equity, the financing process will be different.

The Financing Process

- Credit Check: The dealership will run your credit to determine your eligibility for financing and the interest rate.

- Trade-in Valuation: The dealership will appraise your current car.

- Offer Presentation: They will present an offer for your trade-in, detailing the payoff amount and any negative equity.

- New Car Offer: They will then present a price for the new car, including taxes, fees, and any negative equity from your trade-in.

- Negotiation: This is where you negotiate the price of the new car and the terms of the deal.

- Financing Agreement: If you agree on terms, you’ll sign the paperwork for the new loan.

Tips for Securing Favorable Financing

- Improve Your Credit Score: If possible, work on improving your credit score before applying for a new loan.

- Get Pre-Approved: Obtain pre-approval from your bank or credit union before visiting dealerships. This gives you a benchmark interest rate and strengthens your negotiation position.

- Down Payment: Even if you have negative equity, any additional down payment you can make on the new car will reduce the overall loan amount and potentially secure a better interest rate.

What Happens to the Negative Equity?

The negative equity doesn’t simply disappear. It must be accounted for in one of two ways:

- Paid Out-of-Pocket: You pay the difference in cash.

- Rolled into the New Loan: The shortfall is added to the principal balance of your new car loan.

Table: Impact of Rolling Negative Equity into a New Loan

| Feature | Scenario 1: No Negative Equity | Scenario 2: With Negative Equity Rolled Over |

|---|---|---|

| New Car Price | $30,000 | $30,000 |

| Trade-in Value | $15,000 | $10,000 |

| Loan Payoff | $12,000 | $15,000 |

| Negative Equity | $0 | $5,000 |

| New Loan Amount | $15,000 | $20,000 ($15,000 + $5,000) |

| Estimated Monthly Payment (over 60 months at 5% APR) | ~$283 | ~$377 |

| Total Interest Paid | ~$1,000 | ~$2,600 |

Note: These are illustrative figures and actual payments may vary.

As you can see, rolling over negative equity significantly increases your loan amount, monthly payments, and the total interest paid.

When is it Worth it to Trade In with Negative Equity?

There are specific situations where pursuing a trade-in despite negative equity might make sense:

- Safety Concerns: If your current car is unsafe and repairs would be more costly than the negative equity.

- Unreliable Vehicle: If your car is constantly breaking down, leading to expensive repairs and inconvenience.

- Changing Needs: If your lifestyle has changed (e.g., need a larger vehicle for family or work) and your current car no longer fits.

- Significant Improvement in New Car: If the new car offers substantial improvements in fuel efficiency, reliability, or technology that offset the cost of negative equity.

Frequently Asked Questions (FAQ)

Q1: Can I trade in my car if I still owe money on it?

Yes, you can trade in a car even if you still owe money on it. If your trade-in value is less than your loan payoff amount, you have negative equity.

Q2: What happens if my trade-in value is less than my loan payoff?

The difference between your loan payoff amount and your car’s trade-in value is your negative equity. This amount will typically need to be paid out-of-pocket or rolled into your new car loan.

Q3: How do I find out how much I owe on my car loan?

Contact your lender directly and ask for your loan payoff statement. This statement will detail the exact amount needed to pay off your loan in full.

Q4: Is it a bad idea to roll negative equity into a new car loan?

Generally, it’s not ideal because it increases your new car’s loan amount, your monthly payments, and the total interest you’ll pay over the life of the loan. It also makes it more likely you’ll have negative equity again in the future. However, there can be specific circumstances where it might be a necessary or calculated risk.

Q5: Can I negotiate the negative equity amount?

You can negotiate the overall deal, which indirectly affects how the negative equity is handled. Your negotiation power lies in getting the best possible trade-in value for your current car and the best price for the new car. Some dealerships may have programs or flexibility to help absorb some of the negative equity, especially if you’re buying a higher-priced vehicle.

Q6: What if my car is totaled in an accident, and I have negative equity?

If your car is totaled and you have negative equity, your insurance payout might not cover the full loan balance. You would be responsible for paying the remaining amount to the lender. If you have GAP (Guaranteed Asset Protection) insurance on your loan, it can cover this difference.

Q7: How can I avoid negative equity in the future?

- Make a Larger Down Payment: The more you put down, the less you finance, reducing the risk of negative equity.

- Choose Cars That Depreciate Slowly: Research vehicles known for holding their value.

- Opt for Shorter Loan Terms: Shorter terms mean you pay off the principal faster and pay less interest.

- Avoid Excessive Add-ons: Expensive dealer add-ons (like extended warranties or paint protection) can quickly depreciate and add to your loan balance.

- Consider Used Cars: Slightly used cars have already undergone the steepest part of their depreciation curve.

By carefully considering your options and preparing thoroughly, you can successfully navigate the process of trading in a car with negative equity and move forward with your next vehicle purchase.