When asking, “How long does finance approval take for a car?”, the answer generally ranges from a few minutes to a few business days. This timeframe can vary significantly based on the lender, your credit history, the dealership, and the specific financing method chosen.

Navigating the process of getting a car loan can feel like a maze. One of the most common questions prospective car buyers have is about the timeline: How long does finance approval take for a car? The answer isn’t a single number, as many factors play a role. While some buyers can secure approval in minutes, others might wait a few business days. This detailed guide aims to demystify the auto financing wait and provide a clear picture of the vehicle financing duration. We’ll explore what influences how long car credit takes, from the initial application to final approval, helping you set realistic expectations and prepare accordingly.

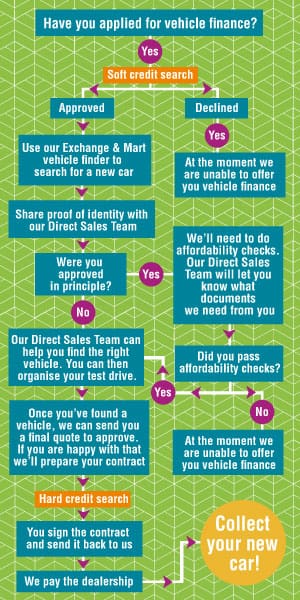

Image Source: www.moneybarn.com

Deciphering the Car Loan Approval Timeline

The journey from wanting a car to driving it off the lot often hinges on securing financing. Understanding the typical car loan approval time is crucial for a smooth purchasing experience. Several stages are involved in the car loan application processing, each contributing to the overall financing turnaround time.

The Initial Application: Your First Step

This is where it all begins. You’ll need to provide information about yourself, your income, employment history, and the vehicle you wish to purchase. The accuracy and completeness of this information are vital. Missing or incorrect details can cause delays.

Credit Checks and Verification: The Deep Dive

Once your application is submitted, lenders will perform thorough credit checks. They’ll look at your credit score, credit history, and debt-to-income ratio. They might also verify your employment and income through pay stubs, bank statements, or by contacting your employer.

Lender Assessment: Weighing the Risks

Lenders assess the risk involved in lending you money. A higher credit score and a stable financial history generally lead to quicker approvals. Conversely, a lower credit score or a history of late payments might require more scrutiny, potentially extending the approval time.

Dealership Involvement: A Key Player

Dealerships often act as intermediaries, working with various lenders to find the best financing for you. Their process can sometimes speed things up, as they have established relationships and streamlined procedures. However, it can also add a layer of complexity.

Types of Financing and Their Timelines

The method you choose for financing significantly impacts how long approval takes.

Dealership Financing Timeline

When you opt for financing directly through the dealership, they typically submit your application to multiple lenders they partner with.

- Instant Approval: For buyers with excellent credit, some dealerships can offer on-the-spot approval. This is often facilitated by pre-approval programs or direct lines of credit with lenders.

- Within a Few Hours: More commonly, dealerships will get a response from a lender within a few hours of submitting your application, especially if it’s a standard business day.

- One to Two Business Days: If your application requires a bit more review, or if it’s submitted late in the day or on a weekend, it might take a day or two for a definitive answer.

Direct Lender Financing Timeline

Applying directly to a bank, credit union, or online lender can sometimes offer a more transparent, albeit potentially longer, process.

- Online Lenders: Many online lenders are highly efficient, offering pre-approval within minutes and final approval within one to two business days.

- Banks and Credit Unions: Traditional banks and credit unions might take a bit longer, especially if you’re not an existing customer. Expect anywhere from one to three business days for approval.

Credit Union Financing

Credit unions are known for their personalized service and often have more flexible approval criteria.

- Quick Approvals: If you’re already a member with a good credit history, you might receive approval relatively quickly, often within the same business day or the next.

- Slightly Longer Wait: For new members or more complex financial situations, the process could extend to two to three business days.

Factors Influencing Approval Speed

Several elements can either accelerate or decelerate the car loan approval time.

Your Credit Score and History

This is arguably the most significant factor.

- Excellent Credit (740+): Typically leads to the fastest approvals, often within minutes or hours. Lenders see you as a low-risk borrower.

- Good Credit (670-739): You can expect approval within a few hours to one business day.

- Fair Credit (580-669): Approval might take one to three business days as lenders may need to scrutinize your application more closely.

- Poor Credit (Below 580): Approval can take several business days, and you might need to explore subprime lenders or options with a co-signer.

Income and Employment Stability

Lenders want assurance that you can repay the loan.

- Stable Employment: A consistent job history, especially in the same field, is viewed favorably.

- Sufficient Income: Your income must be enough to comfortably cover the loan payments and your other expenses.

- Verification: The speed of income and employment verification can impact the overall timeline.

Loan-to-Value (LTV) Ratio

This compares the amount you’re borrowing to the value of the car.

- Lower LTV: A larger down payment means a lower LTV, which reduces the lender’s risk and can speed up approval.

- Higher LTV: Borrowing a higher percentage of the car’s value might require more review.

Down Payment Amount

A larger down payment demonstrates financial commitment and reduces the loan amount.

- Significant Down Payment: Can often lead to faster approvals as it lowers the lender’s risk.

- No Down Payment: While possible, it might lead to longer review periods for approval.

Type of Lender

Different lenders have different operational speeds and risk appetites.

- Online Lenders: Often boast faster, automated processes.

- Dealerships: Can be quick due to established relationships, but might have more paperwork.

- Banks/Credit Unions: Traditional institutions might have more manual processes, potentially leading to a slightly longer vehicle financing duration.

Completeness of Application

As mentioned earlier, a complete and accurate application is key.

- Missing Information: Any gaps in your application will require follow-up, delaying the process.

- Accurate Details: Double-checking all provided information before submission can prevent setbacks.

Current Economic Conditions

Broader economic factors can sometimes influence lending practices and approval times. During economic downturns, lenders might become more cautious, potentially extending approval timelines.

The Pre-Approval Advantage: Accelerating Your Car Search

Seeking car loan pre-approval before you even step into a dealership can be a game-changer for the financing turnaround time.

What is Car Loan Pre-Approval?

Pre-approval is a conditional commitment from a lender to lend you a specific amount of money at a particular interest rate, based on a preliminary review of your finances. It’s not a guarantee, but it’s a strong indicator of your borrowing power.

Benefits of Pre-Approval:

- Knowing Your Budget: You’ll know exactly how much you can afford to spend on a car, allowing you to focus your search.

- Saving Time at the Dealership: Having pre-approval means you can bypass some of the initial financing steps at the dealership, potentially shortening the overall auto financing wait.

- Negotiating Power: Pre-approval shows you’re a serious buyer and can give you leverage to negotiate a better price or interest rate.

- Faster Final Approval: The lender has already done much of the preliminary work, making final approval quicker once you’ve chosen a vehicle. The car loan pre-approval time itself can vary, but often it’s within a few hours to a couple of business days.

Understanding Conditional Car Loan Approval

Sometimes, you might receive a conditional car loan approval. This means the lender has approved your loan, but there are specific conditions you must meet before the funds are disbursed.

Common Conditions:

- Proof of Income: Providing recent pay stubs or tax returns.

- Verification of Employment: Confirming your job status.

- Valid Driver’s License: A requirement for all car loans.

- Proof of Insurance: You’ll need to show you have insurance on the vehicle.

- Specific Vehicle Requirements: The lender may have requirements regarding the age or mileage of the car you’re purchasing.

What Happens Next?

Once you meet these conditions, the lender will finalize the loan. This is typically a quick process, often taking less than a business day. The dealership financing timeline will then move towards finalizing the paperwork and vehicle handover.

Comparing Financing Timelines: A Snapshot

To help visualize the average car loan approval time, consider this general comparison:

| Lender Type | Typical Approval Time (Minutes to Hours) | Typical Approval Time (1-2 Business Days) | Potential Approval Time (3+ Business Days) |

|---|---|---|---|

| Online Lenders | ✓ (Pre-approval) | ✓ (Final approval) | |

| Dealership Financing | ✓ (For excellent credit) | ✓ (Most common) | ✓ (Complex cases) |

| Credit Unions | ✓ (For members with good credit) | ✓ | ✓ (New members/complex cases) |

| Traditional Banks | ✓ | ✓ (New customers/complex cases) |

What is the Average Car Loan Approval Time?

The average car loan approval time can be quite broad, but for most applicants with good credit applying through a dealership or an online lender, it falls between 2 hours and 2 business days. For those with less-than-perfect credit or applying through more traditional channels, it could stretch to 3-5 business days.

Tips for Expediting Your Car Loan Approval

Want to speed up the process of how long car credit takes? Here are some actionable tips:

1. Gather Your Documents in Advance

Having all necessary paperwork ready can significantly reduce delays. This includes:

- Proof of Identity (Driver’s license, passport)

- Proof of Income (Recent pay stubs, W-2s, tax returns)

- Proof of Address (Utility bills, bank statements)

- Employment Verification (Employer contact information)

- Information about existing debts

2. Improve Your Credit Score

If you have time before you need the car, focus on improving your credit score.

- Pay down existing debt.

- Make all payments on time.

- Avoid opening new credit accounts just before applying.

3. Get Pre-Approved

As discussed, pre-approval is a powerful tool to streamline the process.

4. Be Realistic About What You Can Afford

Applying for a loan that’s beyond your means will likely result in denial or a lengthy back-and-forth.

5. Consider a Co-signer

If your credit history is weak, a co-signer with good credit can help expedite approval and secure better terms. However, ensure your co-signer fully understands their responsibility.

6. Shop Around for Lenders

Don’t just stick with the first lender or dealership offer. Comparing offers can help you find the best terms and potentially a faster approval process.

7. Complete Your Application Accurately and Thoroughly

Double-check every field. Any errors or omissions will require follow-up and extend the car loan application processing.

8. Be Available for Follow-Up Questions

Lenders might have questions or require additional documentation. Promptly responding to these requests is crucial for maintaining momentum.

What to Expect When You Get Approved

Once your car loan approval time has elapsed and you receive approval, the final steps are usually straightforward:

- Review the Loan Offer: Carefully examine the interest rate, loan term, monthly payment, and any associated fees.

- Sign the Paperwork: This includes the loan agreement and other necessary documents.

- Vehicle Insurance: You’ll need to provide proof of insurance for the vehicle.

- Drive Away: Once all paperwork is complete and signed, you can drive your new car off the lot!

Frequently Asked Questions (FAQ)

Q1: Can I get approved for a car loan on the same day?

A1: Yes, it’s possible to get same-day approval, especially if you have excellent credit, have obtained pre-approval, or are applying through a dealership with quick processing times.

Q2: What happens if my car loan is denied?

A2: If your loan is denied, the lender is required to provide you with a reason. You can then work on addressing those issues (e.g., improving your credit score, reducing debt) and reapply or seek alternative lenders.

Q3: How does my credit history affect the car loan approval time?

A3: A strong credit history generally leads to faster approvals because lenders perceive you as a lower risk. A weaker credit history may require more scrutiny, potentially extending the approval timeline.

Q4: Does the type of car affect how long finance approval takes?

A4: Sometimes. Lenders might have specific criteria for older vehicles, high-mileage cars, or certain luxury models. If the car you want falls outside standard lending parameters, the vehicle financing duration might be slightly longer as the lender conducts additional assessments.

Q5: Is applying at a dealership faster than applying directly with a bank?

A5: Not always. Dealerships can be very fast due to their relationships with multiple lenders. However, some online lenders have highly efficient, automated systems that can offer near-instant pre-approvals and quick final approvals. It depends on the specific dealership and lender.

Q6: What is the difference between pre-approval and final approval?

A6: Pre-approval is a preliminary assessment of your borrowing potential, giving you an idea of what you might qualify for. Final approval is the lender’s official commitment to lend you the money after a thorough review of your application and the specific vehicle you’re purchasing.

Q7: Can I finance a car with bad credit?

A7: Yes, it is possible to finance a car with bad credit, but the approval process may take longer, and you might face higher interest rates or require a larger down payment. Exploring specialized lenders or using a co-signer can be beneficial. The car loan application processing for subprime borrowers often involves more detailed verification.

By understanding the factors that influence car loan approval time and by preparing thoroughly, you can make the process of securing auto financing as smooth and efficient as possible.