Image Source: content-images.carmax.com

How Can I Trade My Financed Car For Another Car?

Yes, you absolutely can trade your financed car for another car, even if you still owe money on it. This process is common, and dealerships are well-equipped to handle it. Essentially, the dealership will pay off your existing loan, and the remaining balance, if any, will be rolled into the financing for your new vehicle or you’ll need to cover it upfront.

Navigating the world of car ownership often involves transitions. Perhaps your needs have changed, you’re craving an upgrade, or your current vehicle is no longer meeting your expectations. A frequent question that arises is: “Can I trade in my financed car for another car?” The straightforward answer is yes. You can indeed trade in a car that you are still making payments on. This process, while seemingly complex, is a standard practice in the automotive industry. Dealerships are accustomed to handling these situations and can guide you through the necessary steps. The core idea is that the dealership will pay off your outstanding car loan on your current vehicle as part of the transaction for your new car.

The Mechanics of Trading a Financed Car

When you trade in a financed car, the dealership essentially steps in to settle your outstanding car loan payoff. They will determine the car trade-in value of your current vehicle. This value is the amount the dealership is willing to offer for your car, which is then applied towards the purchase of your new vehicle.

Determining Your Current Car’s Value

The car trade-in value is crucial. It’s what the dealership offers for your current car. This figure isn’t simply pulled out of thin air; it’s based on market research, the car’s condition, mileage, features, and demand. You can get an idea of your car’s value by checking online resources like Kelley Blue Book (KBB) or Edmunds. Knowing this beforehand gives you a negotiating advantage.

The Payoff Amount vs. Trade-In Value

The key to the process lies in comparing your car’s trade-in value with the remaining balance on your car loan. There are two primary scenarios:

-

Positive Equity: If your car’s trade-in value is higher than your outstanding loan balance, you have positive equity. This difference is like a down payment towards your new car. For example, if your car is worth $15,000 and you owe $12,000, you have $3,000 in positive equity that can reduce the price of your next car.

-

Negative Equity: If your car’s trade-in value is lower than your outstanding loan balance, you have negative equity car loan. This means you owe more on the car than it’s worth. For instance, if your car is worth $10,000 but you owe $13,000, you have $3,000 in negative equity. This $3,000 deficit will need to be added to the price of your new car or paid out of pocket. This is often referred to as being “upside down” on your loan.

Scenarios When Trading a Financed Car

Let’s delve deeper into how this plays out in different situations.

Scenario 1: Positive Equity

This is the ideal situation. When your car trade-in value exceeds your car loan payoff, the surplus amount acts as a credit towards your new car purchase.

- Example:

- Your car’s trade-in value: $18,000

- Your outstanding car loan balance: $15,000

- Positive Equity: $3,000

In this case, the $3,000 equity reduces the amount you need to finance for your new car. If your new car costs $30,000, you would only need to finance $27,000 (plus taxes, fees, etc.). This makes your new car purchase more affordable.

Scenario 2: Negative Equity

This is more common and presents a challenge. When you owe more than your car is worth, the difference becomes a debt you must address.

- Example:

- Your car’s trade-in value: $12,000

- Your outstanding car loan balance: $16,000

- Negative Equity: $4,000

The dealership will pay off your $16,000 loan. Since they only offer $12,000 for your car, the remaining $4,000 is a deficit. This $4,000 must be paid in one of two ways:

- Added to your new car loan: The $4,000 will be added to the total amount you finance for your new vehicle. This means you’ll be paying interest on that $4,000 over the life of the new loan, increasing your monthly payments.

- Paid upfront: You can pay the $4,000 difference in cash to the dealership. This avoids paying interest on that amount and results in a lower loan amount for your new car.

When dealing with negative equity, carefully consider the long-term implications of rolling it into a new loan. It can significantly increase your overall borrowing costs.

Steps to Trading Your Financed Car

Here’s a breakdown of the typical process when you’re trading in a car with a loan:

-

Gather Information:

- Your Loan Statement: Obtain your latest loan statement to confirm the exact outstanding balance and any early payoff penalties (though these are rare for car loans).

- Your Car’s Condition: Assess your car’s condition honestly. Note any significant wear and tear, necessary repairs, or outstanding recalls.

- Market Value: Research your car’s estimated car trade-in value using online tools (KBB, Edmunds, NADA). This gives you a realistic expectation.

-

Visit Dealerships:

- Shop Around: Visit multiple dealerships, both new and used car dealerships. Some may offer better trade-in values or financing options than others.

- Test Drive and Negotiate: Find a car you like and begin the negotiation process for the new car purchase. Be prepared to discuss your trade-in separately.

-

The Trade-In Offer:

- Dealership Appraisal: The dealership will appraise your current vehicle to determine its trade-in value.

- The Offer: They will present you with a written offer for your trade-in. This is where you compare their offer to your research.

-

Addressing the Loan:

- Dealership Pays Off Loan: If you accept the offer and proceed with the purchase, the dealership will contact your lender to pay off the remaining car loan payoff. They will handle the paperwork for this.

- Handling Negative Equity: If there’s negative equity, you’ll need to decide whether to add it to your new loan or pay it upfront.

-

Financing the New Car:

- New Car Financing Options: You’ll explore car financing options for your new vehicle. This could involve financing through the dealership, your bank, or a credit union.

- Loan Application: You’ll complete a credit application for the new loan. Your credit score will determine your interest rate.

- Signing the Deal: Once the financing is approved and all paperwork is in order, you’ll sign the contracts for your new car.

Alternatives to Trading In

While trading in a car with a loan is common, it’s not the only option. You might consider these alternatives:

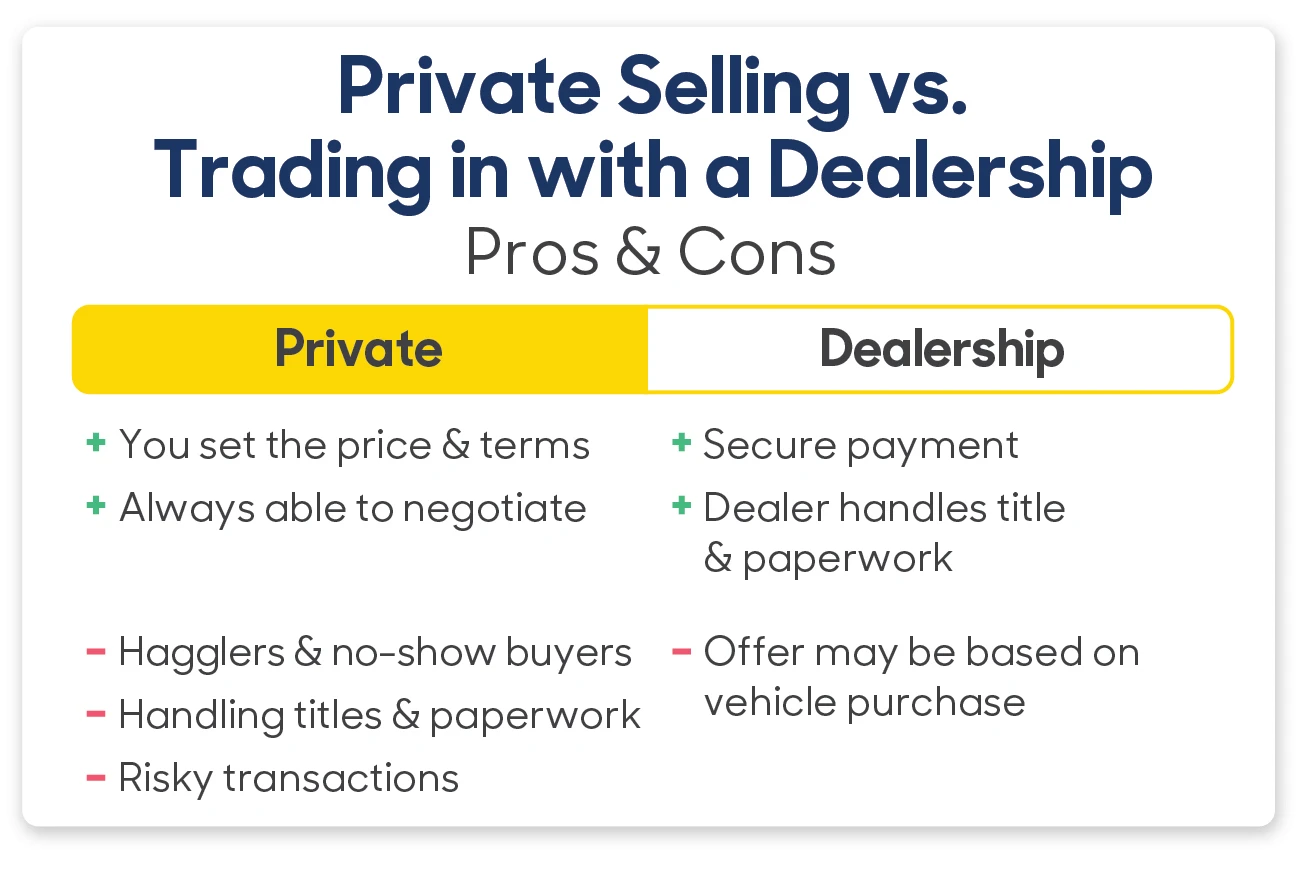

Selling Your Financed Car Privately

Selling financed car yourself can often yield a higher price than a dealership trade-in. However, it’s a more involved process:

- Contact Lender: You’ll need to inform your lender of your intention to sell. They will provide you with the exact payoff amount, including any accrued interest.

- Buyer Pays Off Loan: Ideally, the buyer pays the full agreed-upon price. You then use a portion of that money to pay off your loan, and you provide the buyer with a clear title.

- Handling Negative Equity: If the sale price is less than your loan balance, you’ll need to cover the difference out of pocket before you can transfer the title to the buyer.

- Buyer Financing: If the buyer needs financing, the process can be more complex, often involving a three-way transaction between you, the buyer, and their lender.

Refinancing Car Loan Before Trading

In some cases, you might consider refinancing car loan on your current vehicle to get a lower interest rate or adjust your payment terms. While this doesn’t directly help with trading it in, it can make your existing loan more manageable. If you have positive equity, refinancing might free up some cash or lower your monthly payments, making it easier to manage your finances while looking for a new car. However, refinancing with negative equity can be challenging, as lenders may be hesitant to lend more than the car is worth.

Car Lease Buyout (Not Directly Applicable to Trading a Financed Car)

It’s important to distinguish between trading a financed car and a car lease buyout. A lease buyout occurs when you purchase a vehicle at the end of your lease term. If you are financing a leased vehicle, the process of buying it out is different from trading in a car you own outright but still have a loan on. However, if you have a loan on a car you previously leased and are now looking to trade it in, the principles of trading in a car with a loan still apply.

Factors to Consider When Trading

Before you commit to trading your financed car, weigh these important factors:

- The Cost of Negative Equity: Rolling negative equity into a new loan means you’re paying interest on money you essentially lost. This can significantly increase your monthly payments and the total cost of your new car.

- Depreciation: Cars depreciate rapidly. The longer you keep a car, the less it’s typically worth. If your car has depreciated significantly, you’re more likely to have negative equity.

- Your Financial Situation: Can you afford the increased monthly payments that might come with rolling negative equity into a new loan? Do you have the funds to pay off the difference if necessary?

- New Car Dealership Fees: Dealerships often add various fees and markups. Be sure to scrutinize the final contract and negotiate these where possible.

- Interest Rates: Compare interest rates for your new car financing from different sources (dealership, banks, credit unions) to ensure you get the best deal.

Frequently Asked Questions (FAQ)

Q1: Can I trade my financed car if I have negative equity?

A1: Yes, you can trade your financed car even with negative equity. The negative equity amount will need to be paid, typically by adding it to your new car loan or paying it out of pocket.

Q2: How do I know my car’s trade-in value?

A2: You can get an estimate of your car’s trade-in value from online resources like Kelley Blue Book (KBB), Edmunds, or NADA. Dealerships will also appraise your car.

Q3: What is negative equity car loan?

A3: A negative equity car loan occurs when you owe more on your car loan than the car is currently worth.

Q4: Will a dealership pay off my car loan?

A4: Yes, when you trade in a financed car, the dealership will typically pay off your existing car loan as part of the transaction.

Q5: What are the advantages of trading in my car at a dealership versus selling it privately?

A5: Trading in at a dealership is convenient and simplifies the process, especially when selling financed car. A private sale might fetch a higher price but requires more effort and coordination, particularly if the car is still financed.

Q6: How does refinancing my car loan affect trading it in?

A6: Refinancing your car loan can potentially lower your interest rate or change your payment structure. If you refinance with positive equity, it might free up some funds. However, it doesn’t directly change the fact that the car is financed; the dealership will still pay off the loan when you trade it in.

Q7: What if my car is leased and I want a new car?

A7: If you’re looking to trade in a leased vehicle, the process differs from trading in a car you own with a loan. You would typically go through a car lease buyout process to purchase the car first, and then trade it in. Alternatively, some dealerships may be able to handle the lease payoff directly.

In conclusion, trading in a car with a loan is a common and manageable process. By arming yourself with knowledge about your car’s value, your loan balance, and available car financing options, you can successfully transition to a new vehicle, whether you have positive or negative equity in your current one. Remember to compare offers, understand all costs involved, and make a decision that aligns with your financial goals.